That Settlement Offer Has Nothing to Do With What You Actually Lost

That Settlement Offer Has Nothing to Do With What You Actually Lost

She called me on a Tuesday afternoon, about six weeks after a rear-end collision on Route 9. The adjuster had been “so helpful,” she said. Called within days, sent flowers to her hospital room—I’m not making that up—and had a check ready for $4,200 if she’d just sign a release. She hadn’t signed yet, but she was close. She had a herniated disc, two months of physical therapy ahead of her, and she hadn’t been back to work since the accident.

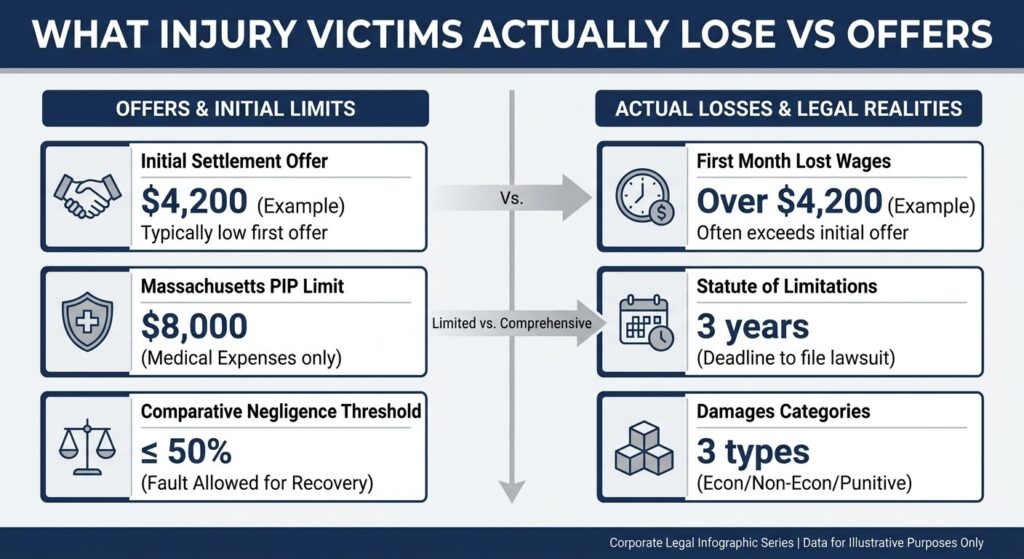

That $4,200 wouldn’t have covered her first month of lost wages.

I see this pattern constantly. Injured people in Massachusetts who don’t know what they’re actually entitled to, who mistake a fast offer for a fair one, and who don’t realize that signing that release closes the door permanently. So let me walk you through what compensation actually looks like under Massachusetts law—not what the adjuster wants you to think it looks like.

What You’re Actually Entitled To: The Full Picture

Massachusetts personal injury law divides recoverable damages into three categories. Most people have heard of two of them. Almost nobody fully understands all three until they’re sitting across from someone who’s spent years watching claims get undervalued.

| Damage Category | What It Covers | How Common |

|---|---|---|

| Economic damages | Medical bills, lost wages, future treatment costs, lost earning capacity | Every claim |

| Non-economic damages | Pain and suffering, emotional distress, loss of enjoyment of life | Every claim |

| Punitive damages | Punishment for willful or malicious conduct | Rare |

Economic damages are the quantifiable losses—the ones with receipts and pay stubs attached. Medical expenses are the most obvious: emergency room bills, surgery costs, imaging, physical therapy, prescription medications, and any future treatment your doctors reasonably expect you to need. Lost wages cover income you couldn’t earn while recovering, and if your injuries affect your earning capacity long-term, that future loss is recoverable too.

Non-economic damages are where most of the confusion—and most of the money—lives. Pain and suffering. Emotional distress. Loss of enjoyment of life. The fact that you can’t coach your kid’s soccer team anymore, or that you wake up at 3 a.m. because your back won’t let you sleep. These are real losses. Massachusetts courts recognize them as real losses. But insurance companies work very hard to convince injured people that these damages are somehow speculative or inflated, because minimizing non-economic damages is how they protect their bottom line.

Punitive damages are rare in Massachusetts personal injury cases. They’re designed to punish defendants for conduct that’s especially egregious—not just negligent, but willful or malicious. What matters for most injured people is building the strongest possible case around economic and non-economic damages.

The distinction between these categories isn’t just academic. It shapes how you document your claim, what evidence you gather, and how you respond when an adjuster makes an early offer. As a personal injury lawyer massachusetts, I’ve watched people leave substantial non-economic damages on the table simply because they didn’t know those damages existed.

Economic Damages: What You Can Prove and How

Medical expenses and lost wages sound straightforward until you’re actually trying to document them.

The no-fault layer most people misread. Massachusetts operates under a modified no-fault insurance system. Massachusetts requires all drivers to maintain PIP coverage under Massachusetts General Laws Chapter 90, Sections 34M and 34N — it pays medical expenses and 75% of lost wages up to $8,000 per person per accident, regardless of fault. Bills get paid early, which creates a false sense that the claim is “handled.” PIP is a floor, not a ceiling. Bills get paid early, which creates a false sense that the claim is “handled.” PIP is a floor, not a ceiling. Once you exhaust PIP and meet the tort threshold, you can pursue the at-fault driver’s liability insurance for the full scope of your damages. Under Massachusetts General Laws Chapter 231, Section 6D, that threshold is met when medical bills exceed $2,000, or when the injury involves a fracture, loss of a body part or significant function, or permanent disfigurement.

Lost wages require real documentation. Pay stubs, employer verification, tax returns if you’re self-employed. If your injury affects your ability to work in the future, you’ll likely need a vocational expert and possibly an economist to project that loss. Insurance companies will push back hard on future lost earning capacity claims—arguing your injury isn’t as limiting as you say, or that you could return to some form of work. This is where having organized records from day one matters enormously.

Future medical costs belong in your claim now. If your orthopedic surgeon says you’ll need a knee replacement in ten years because of this accident, that cost belongs in your claim today. You can’t come back later and reopen a settled case. Settling before you understand the full scope of your medical future is one of the most expensive mistakes I see—and one of the most preventable.

Non-Economic Damages: The Part Adjusters Hope You’ll Forget

There’s no formula that spits out a pain and suffering number. Anyone who tells you otherwise—including any online settlement calculator—is giving you false precision.

Here’s how these damages actually get evaluated:

- Nature and severity of the injury — A spinal injury requiring surgery is valued differently than a soft tissue injury that resolves in six weeks. That’s not unfair; it reflects reality.

- Duration of recovery — Longer recovery periods, especially those involving permanent effects, carry more weight.

- Impact on daily life — What you can no longer do matters. Courts and juries respond to specifics, not generalities.

- Consistency of treatment — Every appointment you skip, every treatment you delay, becomes ammunition for the adjuster.

Emotional distress, loss of consortium (the impact on your relationship with a spouse), and loss of enjoyment of life are all recoverable in Massachusetts. These aren’t soft concepts. They’re recognized categories of harm that courts take seriously. The challenge is presenting them in a way that feels concrete and credible—which is why the details in your own records, journals, and testimony from people who know you matter so much.

What is unfair is when insurance companies treat non-economic damages as a negotiating chip rather than a legitimate category of loss. They’ll point to gaps in treatment, argue you didn’t follow medical advice, or suggest your pain complaints are exaggerated. Consistent medical documentation is your answer to all of it.

Comparative Negligence: The Misconception That Costs People Money

“I can’t recover anything because I was partly at fault.”

That’s wrong. And it costs people real money when they believe it.

Massachusetts follows a modified comparative negligence rule. If you were partially responsible for the accident, your recovery is reduced by your percentage of fault—but you can still recover as long as you were not more than 50% at fault.

A simple example: A jury finds you 25% responsible. Your total damages are $100,000. You recover $75,000. Not zero.

The insurance company knows this. What they’ll try to do is argue your fault percentage is higher than it actually is, because every percentage point they add to your side of the ledger reduces what they owe. They’ll look at whether you were speeding, whether you were distracted, whether you failed to take some action that might have prevented the accident.

This is why what you say to an adjuster in those early conversations matters. Statements get used. Admissions get amplified. If you’re worried about being partly at fault, don’t let that fear push you into a premature settlement—or worse, into not pursuing a claim at all. Get a real assessment of the facts first.

The Statute of Limitations: A Deadline That Does Not Move

Three years from the date of the accident. That’s Massachusetts law for personal injury claims.

Three years sounds like a long time. Here’s what actually happens:

- The first several months go to medical treatment and getting back to some version of normal life.

- Then you start thinking about the claim.

- Then an adjuster keeps you engaged in “negotiations” that go nowhere.

- Then the deadline is approaching and you’re scrambling—or you miss it entirely.

I’ve had those calls. They’re the worst kind.

The three-year clock is a hard stop. With very limited exceptions—claims involving minors, or cases where the injury wasn’t immediately discoverable—courts won’t extend it. Filing even one day late means the defendant can have your case dismissed regardless of how strong it is.

There’s also a practical reason to move earlier rather than later: evidence degrades. Witnesses move or forget details. Surveillance footage gets overwritten. Accident scene conditions change. The strength of your claim is often highest closest to the accident, not three years later.

What the Insurance Company Is Actually Doing

That adjuster who called quickly and seemed so understanding? Their job is to close your claim for as little as possible. That’s not cynicism—it’s the business model. The faster they settle, the less they pay, because injured people who don’t yet know their full prognosis often accept less than their claim is worth.

A few tactics worth knowing:

- Early offers almost never account for future medical expenses or full non-economic damages.

- “How are you feeling?” is not small talk. It’s a question with a purpose, and your answer may be recorded or noted.

- Broad medical authorizations let them search your records for pre-existing conditions to blame your injuries on.

- Recorded statements get used to create inconsistencies between what you said early on and what you say later.

None of this means you can’t navigate a claim without a lawyer. Some people do. But understanding what you’re up against changes how you respond—and that changes what you recover.

Before You Do Anything Else

The to-do list is short but non-negotiable:

- Document everything now. Medical records, bills, pay stubs, photos of your injuries, a daily journal of how you’re feeling and what you can’t do.

- Don’t give a recorded statement without understanding what you’re agreeing to.

- Don’t sign any release without knowing what you’re giving up permanently.

- Don’t wait on the deadline while an adjuster strings you along with promises to “come up” on their offer.

First consultations with personal injury attorneys are typically free. Use that. Get a real assessment of what your claim is worth before you decide whether to settle, negotiate, or file suit.

The offer on the table right now may have nothing to do with what you actually lost. You deserve to know the difference before you sign anything.